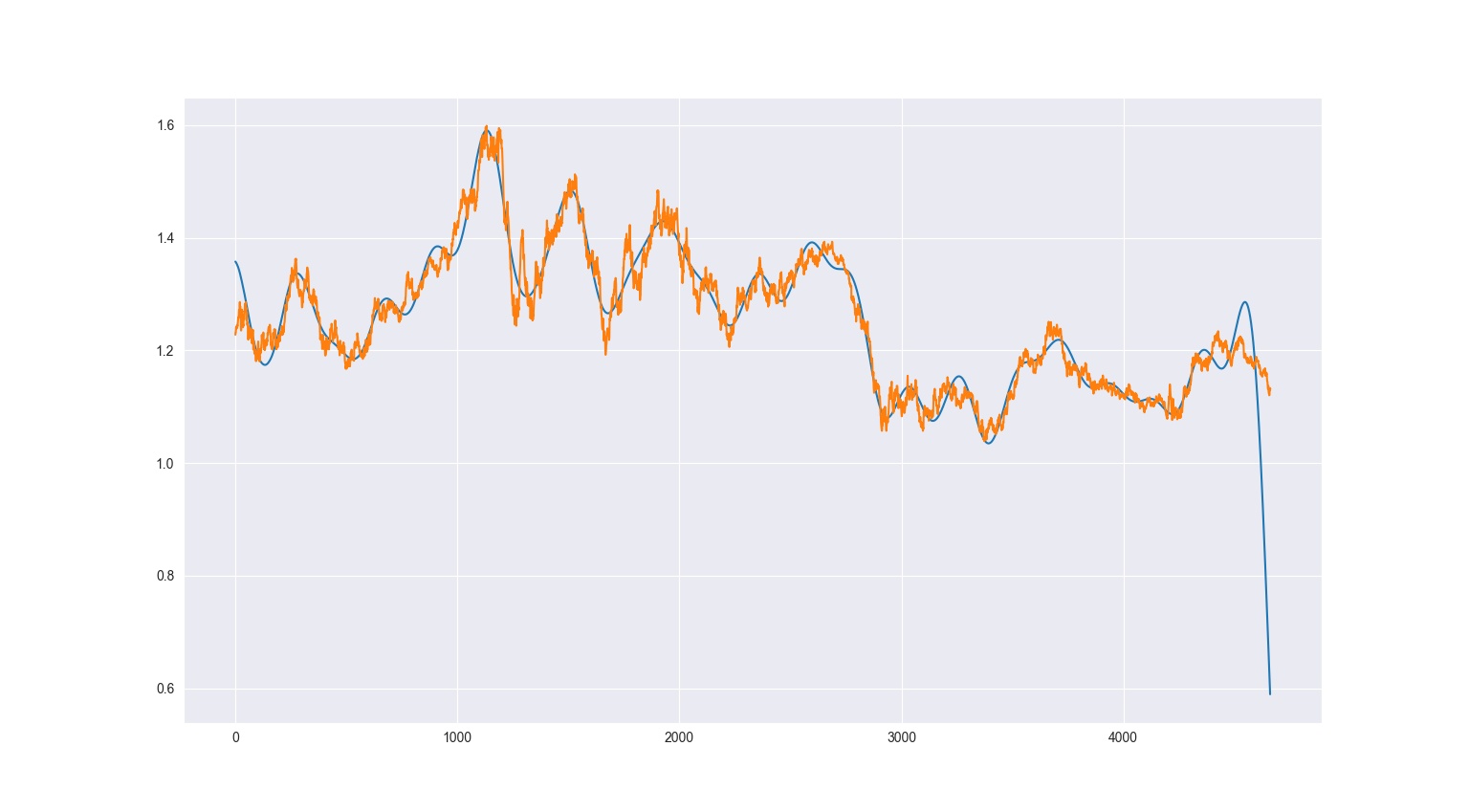

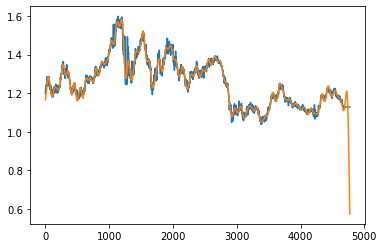

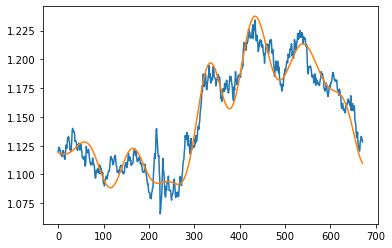

I have performed Hankel Matrix Singular Value Decomposition de-noising to smooth out my univariate time series. It is the close price of EUR/USD exchange rate. Here is a picture:

The problem I have is that the end of the data seems erroneous. How can I fix this or is there a better way to denoise my time series such as a Kalman Filter or wavelet transformation. Here is the main part of my Python code:

import numpy as np

import pandas_datareader as pdr

from datetime import datetime

from scipy.linalg import hankel

import matplotlib.pyplot as plt

symbol = "EURUSD=X"

df = pdr.DataReader(symbol, "yahoo", datetime(2000, 1, 1),

datetime.now()).drop(columns=["Adj Close", "Volume"])

hankel_matrix = hankel(df.Close)

U, S, VT = np.linalg.svd(hankel_matrix)

first_k_singulars = 40

S = [0 if i > first_k_singulars else j for i, j in zip(range(len(S)), S)]

close = U @ np.diag(S) @ VT

max_col = len(close[0])

max_row = len(close)

fdiag = [[] for _ in range(max_row + max_col - 1)]

for x in range(max_col):

for y in range(max_row):

fdiag[x + y].append(close[y][x])

avg_fdiag = []

for i, j in zip(fdiag, range(1, len(fdiag)+1)):

avg_fdiag.append(np.sum(i)/j)

close = avg_fdiag[:len(df)] # take this length of our avg_fdiag as it is a hankel matrix

.csv) and explain the objective. There might be a better to do what you want. $\endgroup$